PX14A6G: Notice of exempt solicitation submitted by non-management

Published on April 30, 2025

United States Securities and Exchange Commission

Washington, D.C. 20549

NOTICE OF EXEMPT SOLICITATION

Pursuant to Rule 14a-103

United States Securities and Exchange Commission

Washington, D.C. 20549

NOTICE OF EXEMPT SOLICITATION

Pursuant to Rule 14a-103

Name of the Registrant: Walmart Inc.

Name of persons relying on exemption: The Shareholder Commons, Inc.

Address of persons relying on exemption: PO Box 1268, Northampton, Massachusetts 01061

Written materials are submitted pursuant to Rule 14a-6(g) (1) promulgated under the Securities Exchange Act of 1934. Submission is not required of this filer under the terms of the Rule, as the filer does not own any securities of the registrant, but is made voluntarily.

Balancing Diversified Shareholder Value and Company Financial Returns

At Walmart, the average hourly wage is not enough to sustain a single adult with no children, even in low-cost areas of the United States. This failure to provide a living wage to people who work for a living threatens the entire economy, and thus the investment portfolios of the average diversified investor.

The Shareholder Commons urges (“TSC”) you to vote “AGAINST” Gregory B. Penner, Chair of the Board (Item 1j on the proxy), due to Walmart’s failure to pay a living wage, which exposes its diversified shareholders’ portfolios to broader economic harm stemming from low wages and income inequality.

TSC is a non-profit advocate for diversified shareholders that works with investors to stop portfolio companies such as Walmart from externalizing costs in ways that can threaten the value of diversified portfolios. TSC addresses the interests of diversified shareholders in optimizing overall market returns.

| 1 |

![]()

Closing the global living wage gap could generate an additional $4.56 trillion in annual economic output through increased productivity and spending.1 This equates to more than a 4% increase in annual global GDP. Inadequate pay, by contrast, imposes a drag on the overall economy’s intrinsic value, which in turn harms investment portfolios reliant on broad economic growth. Walmart has failed to pay a living wage, contrary to its own diversified shareholders’ interests. A vote AGAINST Chair Gregory Penner is thus warranted.

Investors have been asking Walmart for many years to improve its pay practices. TSC filed a shareholder proposal at Walmart last year asking the Company to pay a living wage, with the aim of protecting diversified portfolios from negative effects on the economy caused by inadequate wages and expanding income inequality. Walmart has so far declined to do so. Other shareholders have filed multiple similar proposals through the years seeking improved pay for Walmart’s lowest paid workers. Walmart is the largest employer in the United States;2 its policies thus have tremendous influence on the market as a whole.

Walmart’s opposition to TSC’s proposal last year relied on irrelevant arguments that did not address the magnitude of the threat posed by poverty wages and expanding income inequality:3

| 1. | Walmart said it “provides strong pay and benefits.” But such a statement relied on an irrelevant reference point: while its pay and benefits may allow Walmart to optimize recruiting and retention to meet its internal financial goals, it makes no acknowledgement of the fact that the Proposal addressed the portfolio costs its shareholders absorb from Company wages that fall dramatically short of a living wage. |

| 2. | Walmart said it provides “opportunities for people” to “gain the skills and experiences they need to meet their life and career (including pay) goals.” But while this may be true, it again fails to address the economic damage Walmart creates when it underpays the people to whom it provides “opportunities.” |

| 3. | Walmart said it already operates “in a way that creates substantial value for customers, associates, suppliers, communities, and other constituencies.” But Walmart’s argument did not account for the impact of its low wages on the diversified portfolios of most investors such as Texas teachers, Detroit fire fighters, and other working people who count on their savings and pensions for a dignified retirement. For them, the single greatest determinant of portfolio value is broad economic health, and the living wage gap may be costing the economy $4.56 trillion every year. |

Given Walmart’s history of failure to address its contribution to economic damage arising from an underpaid labor force, a vote AGAINST its board chair is in investors’ best interest.

_____________________________

1 The Business Commission to Tackle Inequality, “Tackling Inequality: The Need and Opportunity for Business Action,” June 2022, https://tacklinginequality.org/files/introduction.pdf.

2 Richard Volpe and Michael A. Boland, “The Economic Impacts of Walmart Supercenters,” Annual Review of Resource Economics 14, no. 1 (October 5, 2022): 43–62, https://doi.org/10.1146/annurev-resource-111820-032827.

3 https://www.sec.gov/ix?doc=/Archives/edgar/data/0000104169/000010416924000078/wmt-20240424.htm

| 2 |

![]()

| A. | Underpaying Workers Threatens Economic Prosperity and Diversified Portfolios |

Low wages and income inequality threaten the global economy with losses that will burden investment portfolios over the next 30 years and beyond, as we explain further in Section C. Conversely, higher wages lead to increased productivity and consumption in a virtuous macroeconomic cycle that benefits investment portfolios.

Diversified investors—including pension funds, foundations, and endowments—and other institutions working on behalf of these investors and other beneficiaries with diversified portfolios must work to bring an end to employment practices at Walmart that threaten the economy upon which their portfolios depend.

In the following sections, we describe the research establishing the relationship between low wages and income inequality on the one hand and long-term returns of diversified portfolios on the other, and show why shareholders can and must steward Walmart away from pay practices that threaten the economy. This system-wide perspective is necessary to protect shareholders, whose diversified portfolios are threatened by company decisions that do not account for systemic effects.

Addressing these systemic concerns means moving beyond the measurement of investment success solely at the company level, and recognizing that portfolio returns are based not only on the profits that companies deliver, but also on the economic impact they create.

| B. | Walmart’s wages are insufficient to mitigate economic damage and do not account for portfolio impact |

Walmart’s wage policies are not sufficient to mitigate the risk its diversified shareholders face to their portfolios from the economic damage that arises from an impoverished workforce and expanding income inequality.

The living wage model reflects “the minimum employment earnings necessary to meet a family’s basic needs while also maintaining self-sufficiency.”4 The living wage is abstemious, making no allowances for savings, consumption of even modest prepared foods, or home purchases, among other things. As the MIT Living Wage Calculator explains:

The living wage is the minimum income standard that, if met, draws a very fine line between the financial independence of the working poor and the need to seek out public assistance or suffer consistent and severe housing and food insecurity. In light of this fact, the living wage is perhaps better defined as a minimum subsistence wage for persons living in the United States.5

_____________________________

4 https://livingwage.mit.edu/pages/about (Living wage is a “market-based approach that draws upon geographically specific expenditure data related to a family’s likely minimum food, childcare, health insurance, housing, transportation, and other basic necessities (e.g. clothing, personal care items, etc.) costs. The living wage draws on these cost elements and the rough effects of income and payroll taxes to determine the minimum employment earnings necessary to meet a family’s basic needs while also maintaining self-sufficiency.”)

5 Ibid.

| 3 |

![]()

Meanwhile, the minimum wage is the lowest legal pay rate companies can offer their employees. Many people believe this is the same as a living wage, but that is not the case. Indeed, in some regions, the chasm between the two is substantial. The U.S. federal minimum wage stood at $7.25 per hour in 2024, whereas the current average living wage in the United States is around $23 per hour for a family of four with both adults working.6 While some states have higher minimums, the highest—Washington, DC’s $17 per hour—still falls well short of a living wage.

| 1. | Walmart’s cost externalization resulting from its failure to pay a living wage |

Walmart says the “average hourly wage for [its] U.S. frontline associates is close to $18.”7 The Company recently reduced its lowest-paid workers’ hourly wage to $13.8 With an average hourly wage that falls well short of a living wage, and a starting hourly wage $10 less than the average living wage, Walmart clearly underpays many of its workers, especially those at starting wages in the lowest-paid jobs.

Walmart’s stores are often located in areas where the cost of living may be lower than national averages. Noting that, we provide in the following table the current living wage for selected Walmart store locations:9

| Store Location | Living wage: 1 adult, 0 children |

Living wage: 2 working adults, 2 children |

| Batesville, MS | $19.23/hour | $21.58/hour |

| Los Lunas, NM | $20.69/hour | $25.90/hour |

| Kuna, ID | $25.67/hour | $30.41/hour |

| Turlock, CA | $23.54/hour | $28.68/hour |

| Flanders, NJ | $28.71/hour | $37.00/hour |

In other words, Walmart’s starting pay is deeply inadequate no matter the employee’s location or family situation, and its average wage fails to meet the basic needs of single, childless employees even in the most economically disadvantaged areas of the country. The average Walmart associate makes far less than necessary to sustain a family of four with both adults working full time, even in locations with the lowest cost of living. Its average hourly wage isn’t even enough to sustain a single adult with no children in the lowest cost-of-living location cited above.

Corresponding to Walmart’s current failure to pay many of its employees a living wage, there is also significant wage inequality within the Company. According to Walmart’s 2025 Proxy Statement, the Company’s CEO made $27 million in the previous fiscal year, or 930 times more than the Company’s median employee.

_____________________________

6 Emma Burleigh, “Americans Are Struggling to Scrape by—More than 40% of Full-Time Workers Aren’t Making a Living Wage,” Fortune, August 26, 2024, https://fortune.com/2024/08/26/many-us-workers-dont-make-living-wage-women-people-of-color/.

7 https://corporate.walmart.com/askwalmart/how-much-do-walmart-associates-make [emphasis added]

8 Daphne Howland, “Walmart Lowers Starting Wage for Some Store Workers,” Retail Dive, September 8, 2024, https://www.retaildive.com/news/walmart-lowers-starting-wage-workers/693071/.

9 See MIT’s Living Wage Calculator at https://livingwage.mit.edu/

| 4 |

![]()

In its Opposition Statement to TSC’s proposal last year, Walmart asserted that its associates who are women or people of color are “paid 1:1 (dollar for dollar)” the pay of their white and male counterparts. We do not dispute that assertion, but it is not responsive to Walmart’s contribution to expanding, economy-wide racial disparity in income: Walmart’s employees of color make up a disproportionate number of employees not earning a living wage because people of color compose more than half the Company’s U.S. workforce, yet account for less than 30 percent of officer roles.10

It appears Walmart’s decision not to pay a living wage is attributable to a Company approach to compensation that does not account for economy- or portfolio-wide risk mitigation, and instead focuses solely on risks to its own business.

| 2. | The broad economic cost associated with poverty wages and income inequality surpasses any risk the issue poses to Walmart itself |

Walmart as a unitary economic force

Walmart is the largest private employer not only in the United States11 but also in the world,12 giving its wages economy-wide impact. With 1.6 million associates in the United States alone,13 more people work at Walmart than the collective populations of 11 U.S. states and the District of Columbia.14 A 2020 research article found that if Walmart were a country, it would rank in the top 25 countries in terms of GDP.15

The term “Walmart Effect” can be traced back to the 1990s.16 In 2006, business journalist Charles Fishman wrote a book titled “The Walmart Effect”17 describing the effects Walmart has on the economy. In 2013, Democratic staff of the U.S. House Committee on Education and the Workforce issued a report titled: “The Low-Wage Drag on Our Economy: Wal-Mart’s low wages and their effect on taxpayers and economic growth.”18 The report raises the issue of cost externalization of Walmart’s low wages: “While employers like Wal-Mart seek to reap significant profits through the depression of labor costs, the social costs of this low-wage strategy are externalized.” And a December 2024 article in The Atlantic, also titled “The Walmart Effect,” highlighted two new research papers that concluded that on net, “Walmart makes the places it operates in poorer than they would be if it had never shown up at all.”19

_____________________________

10 https://corporate.walmart.com/content/dam/corporate/documents/purpose/culture-diversity-equity-and-inclusion-report/2024-annual-belonging-diversity-equity-and-inclusion-annual-report.pdf

11 Richard Volpe and Michael A. Boland, “The Economic Impacts of Walmart Supercenters,” Annual Review of Resource Economics 14, no. 1 (October 5, 2022): 43–62, https://doi.org/10.1146/annurev-resource-111820-032827.

12 https://companiesmarketcap.com/largest-companies-by-number-of-employees/#google_vignette

13 https://corporate.walmart.com/askwalmart/how-many-people-work-at-walmart

14 (Alaska, Delaware, District of Columbia, Hawaii, Maine, Montana, New Hampshire, North Dakota, Rhode Island, South Dakota, Vermont, Wyoming) US Census Bureau, “State Population Totals and Components of Change: 2020-2023,” Census.gov, accessed April 26, 2024, https://www.census.gov/data/tables/time-series/demo/popest/2020s-state-total.html.

15 Robert W. McGee, “How Highly Would Walmart Rank If It Were a Country? A Comparison of Walmart Revenue to Nations’ GDP,” SSRN Scholarly Paper (Rochester, NY, January 22, 2020), https://doi.org/10.2139/ssrn.3524078.

16 Julie Morris, “Store shuts doors on Texas town,” USA Today, October 11, 1990.

17 Charles Fishman, The Wal-Mart Effect: How the World’s Most Powerful Company Really Works - and How It’s Transforming the American Economy (Penguin Books, 2006).

18 Democratic Staff of the U.S. House Committee on Education and the Workforce, “The Low-Wage Drag on Our Economy: Wal-Mart’s Low Wages and Their Effect on Taxpayers and Economic Growth,” May 2013, https://democrats-edworkforce.house.gov/imo/media/doc/WalMartReport-May2013.pdf.

19 Rogé Karma, “The Walmart Effect,” The Atlantic, December 24, 2024, https://www.theatlantic.com/economy/archive/2024/12/walmart-prices-poverty-economy/681122/.

| 5 |

![]()

Generalized impacts of corporate cost externalization from underpaying workers

It has been estimated that a one percent increase in inequality leads to a decrease in GDP of 0.6-1.0 percent.20 A one percent difference in inequality could thus lead to 17-26 percent lower GDP over 30 years and correspondingly lower returns for a diversified portfolio. This means that a 32-year-old worker saving for retirement today through a defined contribution plan could expect to have a nest egg 17-26 percent smaller at age 62. A defined benefit plan facing the same deficit could be forced to lower its benefits significantly, increase employer or employee contributions, or—in the case of a public pension fund—increased tax burdens.

We cover more empirical evidence of the economic damage associated with an underpaid labor force in the next section.

| C. | Poverty wages and income inequality threaten the returns of Walmart’s diversified investors |

| 1. | Investors must diversify to optimize their portfolios |

It is commonly understood that investors are best served by diversifying their portfolios.21 Diversification allows investors to reap the increased returns available from risky securities while greatly reducing that risk.22 This core principle is reflected in federal law, which requires fiduciaries of federally regulated retirement plans to “diversify[] the investments of the plan.”23 Similar principles govern other investment fiduciaries.24

| 2. | The performance of a diversified portfolio largely depends on overall market return |

Diversification is thus required by accepted investment theory and imposed by law on investment fiduciaries. Once a portfolio is diversified, the most important factor determining return will not be how the companies in that portfolio perform relative to other companies (“alpha”), but rather how the market performs as a whole (“beta”). In other words, the financial return to such diversified investors chiefly depends on the performance of the market, not the performance of individual companies. As one work describes this, “virtually all investors have permanent exposure to systematic market risk, which will still determine 75-95% of their return.”25

As shown in the next section, the social and environmental impacts of individual companies such as Walmart can significantly affect beta.

_____________________________

20 Orsetta Causa, Alain de Serres, and Nicolas Ruiz, “Growth and Inequality: A Close Relationship?,” OECD, 2014, https://www.oecd.org/content/dam/oecd/en/publications/reports/2014/06/oecd-yearbook-2014_g1g45233/observer-v2013-5-en.pdf, p. 28.

21 See generally, Burton Gordon Malkiel, A Random Walk down Wall Street: The Time-Tested Strategy for Successful Investing (New York: W.W. Norton & Company, 2020).

22 Malkiel, A Random Walk down Wall Street.

23 29 USC Section 404(a)(1)(C).

24 See Uniform Prudent Investor Act, § 3 (“[a] trustee shall diversify the investments of the trust unless the trustee reasonably determines that, because of special circumstances, the purposes of the trust are better served without diversifying.”)

25 Stephen Davis, Jon Lukomnik, and David Pitt-Watson, What They Do with Your Money How the Financial System Fails Us and How to Fix It (Yale University Press, 2016).

| 6 |

![]()

| 3. | Costs companies impose on social and environmental systems heavily influence beta |

Over long time periods, beta is influenced chiefly by the performance of the economy itself, because the value of the investable universe is equal to the portion of the productive economy that the companies in the market represent.26 Over the long run, diversified portfolios rise and fall with GDP or other indicators of the intrinsic value of the economy. As the legendary investor Warren Buffet puts it, GDP is the “best single measure” for broad market valuations.27

But the social and environmental costs created by companies pursuing profits can burden the economy.28 For example, recent research revealed rising income inequality’s drag on GDP. The increase in income inequality between 1979 and 2018 reduced growth in aggregate demand by about 1.5 percent of GDP. Relative to the 1979 baseline, rising income inequality lowered aggregate demand growth by more than 4 percent annually in the United States.29

Additional research reveals that income inequality and attendant racial and gender disparity harm the entire economy. According to the Economic Policy Institute, income inequality is slowing U.S. economic growth by reducing demand by 2-4 percent.30 The Federal Reserve Bank of San Francisco determined that gender and racial gaps created $2.9 trillion in losses to U.S. GDP in 2019.31 Moreover, a recent report from Citigroup found that had four key racial gaps for Black Americans—wages, education, housing, and investment—been closed in 2000, $16 trillion could have been added to the U.S. economy. Closing those gaps in 2020 could have added $5 trillion to the U.S. economy over the ensuing five years.32 The same study explains steps that corporations could take to reduce the gap. This drag on GDP directly reduces the return on a diversified portfolio over the long term.

_____________________________

26 Richard Mattison, Mark Trevitt, and Liesl van Ast, “Universal Ownership: Why Environmental Externalities Matter to Institutional Investors” (UNEP Finance Initiative and PRI, October 6, 2010), https://www.unepfi.org/fileadmin/documents/universal_ownership_full.pdf, Appendix IV.

27 Warren Buffett and Carol Loomis, “Warren Buffett on the Stock Market,” Fortune Magazine (December 10, 2001), available at https://archive.fortune.com/magazines/fortune/fortune_archive/2001/12/10/314691/index.htm.

28 The Shareholder Commons, “Living Wage & the Engagement Gap: Using a Systems Lens to Build Portfolio Value through Improved Wages,” November, 2023, https://theshareholdercommons.com/case-studies/labor-and-inequality-case-study/.

29 Josh Bivens and Asha Banerjee, “Inequality’s Drag on Aggregate Demand - The Macroeconomic and Fiscal Effects of Rising Income Shares of the Rich” (Economic Policy Institute, 2022), https://www.epi.org/publication/inequalitys-drag-on-aggregate-demand/#:~:text=By%20redistributing%20income%20from%20lower,about%201.5%25%20of%20GDP%20annually.

30 Josh Bivens, “Inequality Is Slowing U.S. Economic Growth: Faster Wage Growth for Low- and Middle-Wage Workers Is the Solution” (Economic Policy Institute, December 12, 2017), https://www.epi.org/publication/secular-stagnation/.

31 Federal Reserve Bank of San Francisco et al., “The Economic Gains from Equity,” Federal Reserve Bank of San Francisco, Working Paper Series, April 7, 2021, 1.000-30.000, https://doi.org/10.24148/wp2021-11.

32 Dana Peterson and Catherine Mann, “Closing the Racial Inequality Gaps: The Economic Cost of Black Inequality in the U.S.” (Citi, September 2020), https://ir.citi.com/%2FPRxPvgNWu319AU1ajGf%2BsKbjJjBJSaTOSdw2DF4xynPwFB8a2jV1FaA3Idy7vY59bOtN2lxVQM=.

| 7 |

![]()

Conversely, closing the living wage gap worldwide could generate an additional $4.56 trillion every year through increased productivity and spending,33 which equates to a more than 4 percent increase in annual GDP.

The reduction in economic productivity caused by income inequality and racial disparity directly reduces returns on diversified portfolios,34 and creates serious social costs that further threaten financial markets. For example, excessive inequality can erode social cohesion and heighten political polarization, leading to social instability.35

Excessive inequality is also a social determinant of health that is linked to more chronic health conditions developed earlier in life, thereby increasing health costs and decreasing the value of human capital.36 A recent study found that “a sustained history of low-wage earning in midlife was associated with significantly earlier and excess mortality, especially for workers whose low-wage earning was experienced in the context of employment instability.”37 Early and excess mortality, in turn, has its own economic costs. Researchers calculated a potential economic output loss of up to 2.6 percent of GDP by 2030 in low-income countries and 0.9 percent in upper-middle-income countries from early and excess mortality.38

A U.S. Government Accountability Office report39 revealed how taxpayers foot the bill when corporations underpay their workers. Millions of full-time workers rely on federal health care and food assistance programs just to get by, and the wholesale and retail trade is in the top five industries with the highest concentration of working adults enrolled in Medicaid and SNAP.40 This, of course, is a form of corporate welfare, in that taxpayers—and, by extension, shareholders—are subsidizing employers who pay low wages.

_____________________________

33 The Business Commission to Tackle Inequality, “Tackling Inequality: The Need and Opportunity for Business Action,” June 2022, https://tacklinginequality.org/files/introduction.pdf.

34 Ibid n.15.

35 International Monetary Fund, IMF Fiscal Monitor: Tackling Inequality (October 2017), available at https://www.imf.org/en/publications/fm/issues/2017/10/05/fiscal-monitor-october-2017.

36 Anne Matusewicz and Henry Mason, “Facing Hard Truths: The Material Risk of Rising Inequality,” Pensions & Investments, September 16, 2020, https://www.pionline.com/sponsored-content/facing-hard-truths-material-risk-rising-inequality.

37 Katrina L. Kezios et al., “History of Low Hourly Wage and All-Cause Mortality Among Middle-Aged Workers,” JAMA 329, no. 7 (February 21, 2023): 561, https://doi.org/10.1001/jama.2023.0367.

38 Blake C. Alkire et al., “The Economic Consequences Of Mortality Amenable To High-Quality Health Care In Low- And Middle-Income Countries,” Health Affairs 37, no. 6 (June 2018): 988–96, https://doi.org/10.1377/hlthaff.2017.1233.

39 United States Government Accountability Office, Federal Social Safety Net Programs: Millions of Full-Time Workers Rely on Federal Health Care and Food Assistance Programs (October 2020), available at https://www.gao.gov/assets/gao-21-45.pdf.

40 Ibid.

| 8 |

![]()

For a full survey of the empirical evidence for the economic damage arising from poverty wages and income inequality, see The Shareholder Commons, “Living Wage & the Engagement Gap: Using a Systems Lens to Build Portfolio Value through Improved Wages,” November, 2023, https://theshareholdercommons.com/case-studies/labor-and-inequality-case-study/.

The acts of individual companies affect whether the economy will bear these costs: if they increase their own bottom line by underpaying workers, the profits earned for and capital returned to their shareholders may be inconsequential in comparison to the added costs the economy bears.

Economists have long recognized that profit-seeking firms will not account for costs they impose on others, and there are many profitable strategies that harm shareholders, society, and the environment.41 Indeed, in 2018, publicly listed companies around the world imposed social and environmental costs on the economy with a value of $2.2 trillion annually—more than 2.5 percent of global GDP.42 This cost was more than 50 percent of the profits those companies reported.

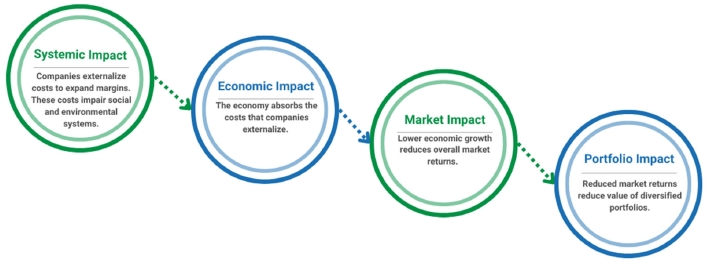

As shown below in Figure 1, Walmart’s choices that contribute to a financially insecure labor force threaten its diversified shareholders’ financial returns, even if those decisions might benefit Walmart financially.

Figure 1

_____________________________

41 See, e.g., Kaushik Basu, Beyond the Invisible Hand: Groundwork for a New Economics, (Princeton University Press, 2011), p.10 (explaining the First Fundamental Theorem of Welfare Economics as the strict conditions (including the absence of externalities) under which competition for profit produces optimal social outcomes).

42 Andrew Howard, “SustainEx: Examining the Social Value of Corporate Activities” (Schroders, April 2019), https://www.schroders.com/en-ch/ch/professional/insights/sustainex-quantifying-the-hidden-costs-of-companies-social-impacts/.

| 9 |

![]()

Walmart’s disclosures demonstrate that its compensation strategy simply fails to address the economic costs of poverty wages and income inequality.

| D. | Why you should vote “AGAINST” the Board Chair |

Voting “AGAINST” the Board Chair will signal to Walmart that shareholders want the Company not to put the economy (and thus their diversified portfolios) at risk.

Additionally:

| · | Walmart underpays its workers, which creates an economy-wide risk that poses a threat to diversified shareholders. |

| · | Walmart’s disclosures show it is not taking the actions that are required of corporations seeking to end practices that externalize costs onto the broader economy and diversified shareholders. |

| · | Walmart’s decision-makers—who are heavily compensated in equity—do not share the same broad market risk as Walmart’s diversified shareholders. |

| E. | Conclusion |

Please vote “AGAINST” Gregory B. Penner, Item 1j.

By voting “AGAINST” Item 1j, shareholders can urge Walmart to account directly for its poverty wages and the resulting costs to society, which in turn affect the economic health upon which diversified portfolios depend. Paying a living wage can aid the Board and management in authentically serving the needs of Walmart’s diversified shareholders and in preventing the dangerous implications—to diversified shareholders and others—of a narrow focus on internal financial return.

The Shareholder Commons urges you to vote “AGAINST” Gregory B. Penner, Board Chair (Item 1j on the proxy), over Walmart’s failure to protect its diversified shareholders’ portfolios by paying a living wage, at the Walmart Inc. Annual Meeting on June 5, 2025.

For questions regarding this exempt solicitation, please contact Sara E. Murphy of The Shareholder Commons at +1.202.578.0261 or via email at sara@theshareholdercommons.com.

THE FOREGOING INFORMATION MAY BE DISSEMINATED TO SHAREHOLDERS VIA TELEPHONE, U.S. MAIL, E-MAIL, CERTAIN WEBSITES, AND CERTAIN SOCIAL MEDIA VENUES, AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE OR AS A SOLICITATION OF AUTHORITY TO VOTE YOUR PROXY.

PROXY CARDS WILL NOT BE ACCEPTED BY THE SHAREHOLDER COMMONS.

TO VOTE YOUR PROXY, PLEASE FOLLOW THE INSTRUCTIONS ON YOUR PROXY CARD.

10